Selling investment property at a loss is never the plan, but sometimes it’s the right choice. If your California property has become more of a financial burden than an asset, you might wonder if there’s any way to recover some of that loss. The good news? The IRS allows certain tax deductions that can help.

Understanding how capital losses work and whether you qualify for a deduction can make a big difference. Not every loss is tax-deductible, but if your investment property meets the right criteria, you could reduce your taxable income and even carry losses forward to future years.

This guide will explain how tax write-offs for investment property work, how to calculate your loss, and what strategies can help minimize your tax bill. We’ll also discuss when selling your property quickly for cash—with Osborne Homes as a hassle-free option—might be the best move.

How the IRS Classifies Investment Property Sales

Before you can understand how capital losses work, it’s important to know how the IRS categorizes the sale of an investment property in California. When you sell, your transaction will fall into one of two tax categories.

Ordinary Income Tax (For Rental Earnings)

If you rented out your property before selling, the income you earned is considered ordinary income and taxed at your regular income tax rate. The good news is that you can deduct property-related expenses like mortgage interest, repairs, property management fees, and depreciation, which helps lower your tax bill.

Capital Gains Tax (For Profits on a Sale)

If you sell your investment property for more than you paid (adjusted for improvements and depreciation), you may owe capital gains tax. The rate you pay depends on how long you held the property.

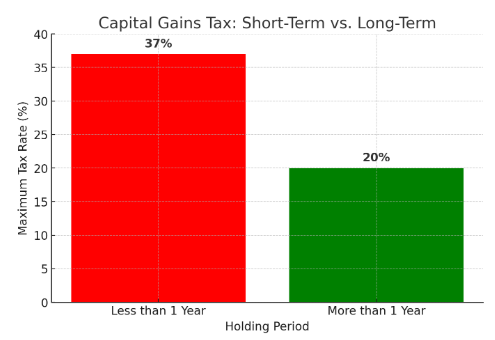

Short-Term vs. Long-Term Capital Gains

The IRS treats profits from the sale of investment property differently depending on how long you owned it before selling.

Short-term gains (less than 1 year)

If you sell an investment property within one year of purchasing it, any profit is taxed at higher short-term capital gains rates—up to 37%, the same as your ordinary income tax rate. Selling too soon can mean paying more in taxes than if you had waited.

Long-term gains (over 1 year)

If you hold onto your investment property for more than a year, you qualify for long-term capital gains tax rates, which are lower—either 0%, 15%, or 20%, depending on your taxable income. This tax advantage is why many investors wait at least a year before selling.

Capital Gains Tax: Short-Term vs. Long-Term

To illustrate the difference, here’s a simple comparison:

Holding onto your property for at least a year can lead to significant tax savings. If you’re thinking about selling, timing it right could make a big difference.

How to Determine if You Can Deduct Your Loss

If you sell an investment property for less than what you originally paid, you may be able to deduct the loss from your taxes. But first, you need to determine whether you qualify for a capital loss deduction.

Step 1: Calculate Your Adjusted Basis

The IRS calculates your loss based on your property’s adjusted basis, which is different from just the original purchase price.

Here’s the formula:

Purchase Price + Cost of Improvements – Depreciation Claimed = Adjusted Basis

For example:

- You bought a rental property for $500,000.

- You put $100,000 into renovations.

- You claimed $50,000 in depreciation deductions over the years.

- Your adjusted basis is $550,000.

- If you sell for $450,000, your capital loss is $100,000.

Step 2: Make Sure It’s an Investment Property

The IRS only allows capital loss deductions for investment properties. If you’re selling a primary residence, your loss won’t qualify for a tax deduction.

Step 3: Apply Your Loss Against Other Income

If your loss qualifies, you can use it to offset capital gains from other investments, like another property or stocks. If you don’t have enough gains to offset, you can deduct up to $3,000 per year against your regular income, carrying forward the rest into future tax years.

Know Your Tax Liability Before You Sell

Curious about how much you might owe in capital gains taxes? Don’t guess—get a clear estimate before making your next move. Use our Capital Gains Calculator to see your potential tax liability and make an informed decision about selling your investment property in California.

Calculate Your Capital Gains Now

The Hidden Tax Rule That Catches Many Sellers Off Guard

Many property owners assume that selling at a loss means no taxes. But there’s one rule that can still affect your tax bill: depreciation recapture.

What Is Depreciation Recapture?

When you own a rental property, you get tax benefits from depreciation deductions. However, when you sell, the IRS recaptures some of those tax savings—even if you sell at a loss.

For example:

If you deducted $50,000 in depreciation, the IRS recaptures that amount at 25%, meaning you owe $12,500 in taxes on depreciation—even if the sale was at a loss.

Many sellers don’t realize they could still owe taxes, so it’s important to factor this into your decision when selling an investment property in California.

Smart Tax Strategies to Make the Most of Your Loss

If you’re selling your property at a loss, here are a few ways to minimize the impact.

Offset Your Gains

If you profited from stocks, another property sale, or a business this year, your real estate loss can help cancel out those gains. This strategy lowers your taxable income, reducing the amount you owe in taxes for the year.

Carry Over Excess Losses

If your capital loss exceeds your gains, the IRS lets you deduct up to $3,000 per year against ordinary income. Any remaining losses roll over to future years, allowing you to continue reducing your taxable income over time.

Consider a 1031 Exchange

A 1031 exchange lets you reinvest in another investment property without immediately paying capital gains taxes. This strategy works well for investors planning to stay in real estate, as it allows tax deferral while continuing to grow your portfolio.

Convert to a Primary Residence

According to the State of California Franchise Tax Board, if you live in your investment property for at least two years before selling, you could qualify for a capital gains tax exemption of up to $250,000 if you’re single or $500,000 if married and filing jointly. This means you won’t have to pay taxes on that portion of your profit.

To qualify, you must meet the ownership and use requirements, which means:

- You owned the home for at least two years within the five years before selling.

- You lived in the home as your primary residence for at least two years during that same five-year period.

- You haven’t used this exclusion in the last two years for another property.

This exemption applies to various types of homes, including houses, condos, mobile homes, trailers, and even houseboats. However, if your gain exceeds the exemption limit, the amount over $250,000 (or $500,000 for couples) will be subject to capital gains tax.

If you don’t qualify for the exemption, you’ll need to calculate your gain and report it on your tax return using IRS Form 1040 Schedule D and California Schedule D (540) for state tax reporting.

When Holding Onto Your Investment is No Longer Worth It

Sometimes, waiting for the market to improve isn’t the best choice. If your property is draining your finances and no longer worth keeping, selling now might be the smartest move. Here are some signs that it is time to sell.

The property is no longer profitable

If your property is costing more in taxes, repairs, and upkeep than it’s bringing in through rental income or appreciation, it may not be worth holding onto. Selling now could prevent further financial strain and ongoing losses.

Repairs and maintenance are adding up

If your property needs constant repairs or major renovations to remain livable or competitive in the market, the costs can quickly outweigh any future profit. Selling as-is might be a smarter financial decision than investing more money.

You need cash now

If you’re facing financial difficulties or need quick access to funds for another opportunity, waiting months for a traditional home sale may not be an option. Selling for cash can provide immediate relief and financial flexibility.

Tenant issues are becoming too much

Dealing with difficult tenants, late payments, vacancies, or legal disputes can be exhausting and costly. If managing the property is becoming more of a hassle than it’s worth, selling could be a stress-free way to move forward.

Ready to Cut Your Losses? Sell Without the Hassle

Selling investment property at a loss isn’t ideal, but holding onto a bad investment can be even worse. Between ongoing expenses, property taxes, and market uncertainty, waiting too long to sell could cost you more in the long run.

Can you write off loss on sale of investment property? Yes, and Osborne Homes makes it simple. We buy houses as-is, so there’s no need for repairs, listings, or waiting on a buyer. We handle everything and close fast, so you don’t have to worry about buyer financing falling through.

If you’re ready to move on without the hassle, let’s talk. Call us today or request a cash offer now!

Get a Cash Offer Now